Transitioning to IFRS (International Financial Reporting Standards) represents a major strategic project for groups. These international accounting standards, adopted by over 140 countries, aim to harmonize financial statement presentation and improve their transparency, comparability and reliability. In Europe, IFRS adoption has been mandatory for companies listed on a regulated market since 2005 (EC Regulation No. 1606/2002). Many unlisted companies also voluntarily adopt IFRS, for example to attract investors or prepare for an IPO, as IFRS are a mark of quality and facilitate access to international financing.

However, an unlisted group retains the option to keep local standards for its consolidated accounts. In France, individual statutory accounts must remain under French accounting standards (French GAAP) — IFRS are not permitted — which requires producing specific restatements for IFRS consolidation purposes. IFRS adoption is therefore a strategic decision to be carefully considered, with advantages in terms of comparability and credibility, but also significant costs and technical complexity.

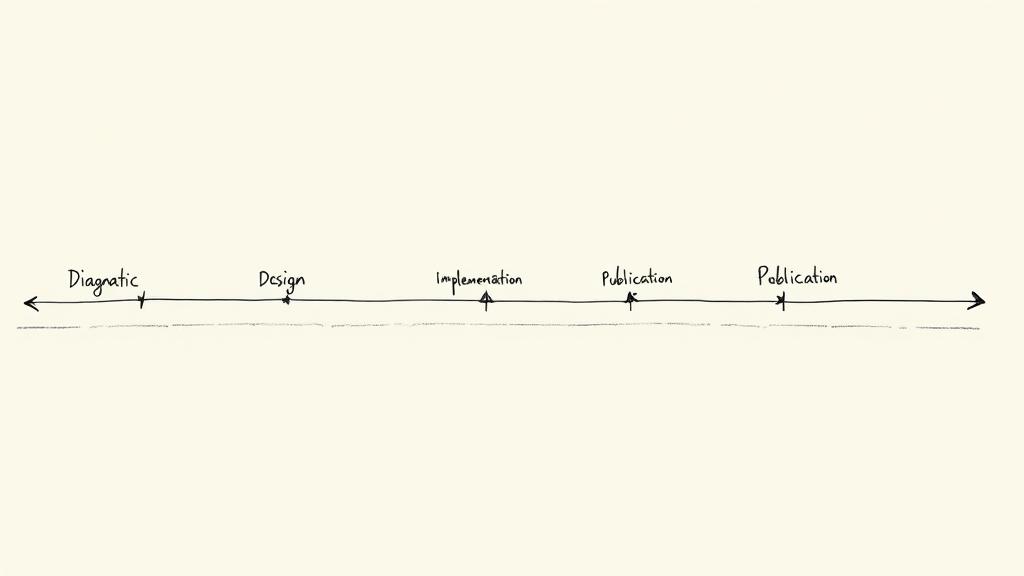

This practical guide presents the key steps to successfully carry out an IFRS transition project. Typically, such a project breaks down into four major phases: Diagnostic, Design, Implementation and Publication.

| Phase | Objective | Key Deliverables | Indicative Duration |

|---|---|---|---|

| 1. Diagnostic | Map gaps between local GAAP and IFRS | Gap matrix, impact estimates, project plan | 2 to 4 months |

| 2. Design | Define accounting options and target processes | IFRS accounting manual, chart mapping, training plan | 3 to 6 months |

| 3. Implementation | Adapt systems and train teams | System configuration, pilot closes, training materials | 6 to 12 months |

| 4. Publication | Produce the first IFRS financial statements | IFRS financial statements, reconciliation schedules, audit report | 3 to 6 months |

Phase 1 — Diagnostic: Gap Analysis and Impact Identification

The first step of an IFRS project is to conduct a full diagnostic of the company's current accounting framework against IFRS standards. The objective is to map the gaps and measure potential impacts on the group's financial statements. This preliminary diagnostic can be completed within a few weeks with expert support.

In practice, this involves comparing current accounting principles (for example France's CRC 99-02 framework) with IFRS requirements, standard by standard. This gap analysis identifies the major accounting areas impacted: financial instruments, revenue recognition, lease contracts, intangible assets, etc. One can expect the recognition of new assets or liabilities (lease obligations under IFRS 16, capitalization of development costs under IAS 38) and measurement changes (fair value for certain financial instruments under IFRS 9, component depreciation under IAS 36).

| Standard | Domain | Typical Impact |

|---|---|---|

| IFRS 1 | First-time adoption | Opening balance sheet, optional exemptions |

| IFRS 3 | Business combinations | Elimination of goodwill amortization |

| IFRS 9 | Financial instruments | Classification and fair value measurement |

| IFRS 15 | Revenue from contracts | 5-step revenue recognition model |

| IFRS 16 | Leases | Right-of-use asset recognition on balance sheet |

| IAS 16 | Property, plant & equipment | Component approach, revaluation option |

| IAS 19 | Employee benefits | Actuarial valuation of pension obligations |

| IAS 36 | Impairment of assets | Annual impairment tests (goodwill, CGUs) |

| IAS 38 | Intangible assets | Capitalization of development costs |

Assessing Project Scope and Preparing Next Steps

The diagnostic also aims to identify the transition effort required, anticipate resource needs (human, budgetary, information systems) and develop an initial conversion timeline. This step should result in defining the project scope and plan: which group entities are concerned, what IFRS transition date will be selected, and what is the work schedule through to the first publication.

Consulting Insight

The transition date corresponds to the beginning of the first period presented as comparative in the IFRS financial statements. In other words, for a first publication at December 31 Year N, the IFRS opening balance sheet must be prepared at January 1st Year N-1. For example, the Sword group prepared an opening balance sheet at January 1st 2004 to carry out its first IFRS consolidation in 2005, this opening balance sheet being the starting point for applying standards in accordance with IFRS 1.

Involving senior management (Chief Financial Officer (CFO), audit committee) and the statutory auditors from this phase is non-negotiable. The potential impact on key financial indicators (net income, shareholders' equity, banking covenants) must be communicated and anticipated at the highest level. Auditors will audit the first IFRS financial statements; validating with them the scope of identified gaps and the planned restatement methodology is therefore advisable.

Phase 2 — Design: Defining Accounting Options and Processes

Once the diagnostic is completed and the decision to adopt IFRS is made, the design phase aims to define precisely how the company will carry out this transition. This involves first choosing accounting methods and options offered by the standards, then defining the new processes and tools required.

Choosing Accounting Methods and Options

IFRS allow, in certain areas, a choice between several accounting methods. Defining the IFRS accounting policies the group will adopt during this phase is a structuring decision, consistent with its strategy and industry practices:

- Property, plant and equipment: cost model or fair value revaluation (IAS 16 / IAS 38)

- Investment property: cost model or fair value (IAS 40)

- Goodwill: under IFRS, no more systematic amortization; annual impairment tests (IFRS 3)

Consulting Insight — IFRS 1 Options

IFRS 1 (First-time Adoption of IFRS) provides exemptions to avoid certain retrospective restatements that would be too costly. For example, IFRS 1 allows not restating pre-transition acquisitions under IFRS 3 — an option chosen by the Sword group, which did not restate acquisitions made before January 1st 2004. Similarly, IFRS 1 offers the possibility to reset cumulative translation differences at the transition date. All first-time application options should be reviewed and these choices formalized in the group's IFRS accounting manual.

Designing New Processes

Switching to IFRS often requires evolving accounting and financial processes to collect additional data and apply new treatments:

- Asset components (IAS 16): allocating acquisition cost by component in the accounting system

- Lease contracts (IFRS 16): inventorying all current leases and collecting data (rents, maturities, discount rates)

- Revenue recognition (IFRS 15): tracking contract performance progress, distinguishing multiple performance obligations

- Financial instruments (IFRS 9): establishing procedures to obtain fair values on a recurring basis

The chart of accounts and reporting formats must also be redesigned to adapt to the IFRS format. Under French GAAP, exceptional income and expenses are isolated, while this concept does not exist under IFRS; conversely, IFRS distinguish items presented in "other comprehensive income" (OCI). An accounting mapping and standardized restatement tables must be defined to bridge from local statutory accounts to IFRS consolidated accounts.

Finally, the design phase includes preparing the training and change management plan. IFRS training needs for the teams should be identified, along with an internal (and external if necessary) communication strategy to explain upcoming changes.

Phase 3 — Implementation: System Adaptation and Team Training

The third phase involves the concrete implementation of previously defined changes. This means deploying new processes, adapting information systems, performing accounting restatements and training teams.

Information Systems Adaptation

One of the most technical aspects of IFRS transition is modifying or configuring accounting and consolidation software to integrate the new rules. In France, as individual accounts must remain under French GAAP, there will often be a coexistence of two frameworks: subsidiaries record under local standards and submit consolidated packages with IFRS restatements. This dual-framework period demands great rigor to avoid inconsistencies and information loss.

If the group did not already have a powerful consolidation tool, the IFRS transition may be an opportunity to invest in a more capable one. Specialized tools may also be deployed: lease management software for IFRS 16, hedging management modules for IAS 39 / IFRS 9.

Consulting Insight

Extensive testing and validation should be performed. Pilot closes or "dry runs" under IFRS allow the process to be refined before the official deadline. For example, the group may prepare IFRS financial statements for an interim period (quarter or half-year) of the fiscal year preceding effective adoption, to identify difficulties and correct them in advance.

Training and Team Mobilization

The success of an IFRS project largely depends on upskilling accounting and finance teams. A training plan covering the head office consolidation team as well as subsidiary accountants and controllers is recommended. Everyone must understand the key IFRS principles and the changes from previous practices.

Beyond technical training, operational teams and other departments must be involved:

- Operational teams: process adaptation (contract unbundling, inventory tracking for fair value)

- Information technology (IT) department: support for system changes

- Tax team: anticipating tax impacts of new treatments

- Management control: adapting performance indicators

A steering committee meeting regularly to track progress across workstreams (IT, accounting, training), address blocking points and ensure schedule compliance is strongly recommended.

For listed companies, gradual external communication is often required during the transition period. European securities regulators recommended a phased information approach during the 2005 IFRS transition, encouraging issuers to provide impact information as early as 2004 and to present interim 2005 accounts under IFRS in parallel.

Phase 4 — Publication: First IFRS Consolidation

The final step corresponds to the publication of the first IFRS financial statements. This is the culmination of all previous work.

Preparing Complete IFRS Financial Statements

IFRS 1 requires that the first annual financial statements published under IFRS include a comparative period also prepared under IFRS. In practice, this means presenting not only the current year's statements, but also restating the prior year under IFRS to show it as comparative.

The financial statements to be published include the full set of primary statements in IFRS format:

- Balance sheet (statement of financial position)

- Income statement and statement of comprehensive income

- Cash flow statement

- Statement of changes in equity

- Notes (explanatory disclosures)

Particular attention must be paid to presentation compliance (adherence to IAS 1) and completeness of disclosures. IFRS require extensive descriptive and quantitative information: accounting policies adopted, estimation assumptions, related party transactions, operating segments (IFRS 8), fair values (IFRS 13).

Reconciliation Statements and Gap Explanations

IFRS 1 explicitly requires presenting reconciliation statements between the previous framework and IFRS:

- Reconciliation of shareholders' equity (previous GAAP to IFRS) at the transition date and at the end of the comparative period

- Reconciliation of net income for the comparative period

- Standard-by-standard explanation of each gap with quantified impact

Consulting Insight

In its first IFRS communication, the Sword group published a complete set of bridge statements between French GAAP and IFRS accounts, accompanied by explanatory notes detailing the transition impact for each standard. It is recommended to segment effects by major theme (fair value measurement, consolidation and scope, financial instruments, provisions and liabilities) and to provide qualitative commentary alongside raw figures.

Validation and Final Communication

Before finalizing IFRS accounts, a final audit by the statutory auditors is necessary. Once the audit is completed without qualification, the group can publish its IFRS consolidated accounts. Financial communication should highlight the main changes resulting from the IFRS transition and quantify their impacts: increased profit due to goodwill amortization cessation, decreased earnings before interest, taxes, depreciation and amortization (EBITDA) due to IFRS 16, etc.

After the initial publication, the company must remain vigilant during the post-transition period. On one hand, dual frameworks must be maintained if local obligations require it. On the other, a monitoring process should be established to track IFRS developments (for example the upcoming IFRS 18 standard on financial statement presentation expected around 2027).

Practical Advice by Company Profile

Each IFRS transition project has specificities depending on company size, listed status, industry and organizational structure.

| Profile | Top Priority | Critical Standards | Recommended Timeline |

|---|---|---|---|

| Listed Group | Regulatory compliance and market communication | IFRS 1, IAS 1, IFRS 8 | 18 to 24 months |

| Unlisted Mid-Cap | Strategic cost/benefit trade-off | IFRS 15, IFRS 16, IAS 19 | 12 to 18 months |

| Financial Sector | Specialized technical standards | IFRS 9, IFRS 17 | 24 to 36 months |

| Industry / Commerce | Impact on debt and revenue | IFRS 15, IFRS 16, IAS 36 | 12 to 18 months |

| Subsidiary of IFRS Group | Consistency with parent group options | Per parent group | 6 to 12 months |

Groups Listed on a Regulated Market

For listed companies, IFRS transition is not optional but a legal requirement. Start the diagnostic at least two years before the first application deadline. Communicate in annual reports preceding the transition on progress and expected impacts. Anticipate market expectations: analysts and investors must be informed of any significant impact. Finally, follow specific recommendations from securities regulators (French Financial Markets Authority (AMF), European Securities and Markets Authority (ESMA)).

Mid-Sized Unlisted Companies

For an unlisted group, IFRS adoption is optional and must be justified by a clear strategic need (attracting international investors, facilitating an acquisition, preparing for an IPO). If such prospects exist, the benefits can outweigh the costs. Otherwise, deferring is reasonable. Note that the IFRS for small and mid-sized enterprises (SMEs) standard is not endorsed in Europe: it is either full IFRS or nothing.

Financial Sector Companies

Banking and insurance groups must be aware of the additional complexity in their sector. Specific standards such as IFRS 9 (financial instruments) for banks or IFRS 17 (insurance contracts) are among the most technical in the framework. Specialized expertise (actuaries, risk specialists) must be mobilized, and the project should be broken down into standard-specific workstreams with dedicated teams.

Industrial and Commercial Companies

Focus the analysis on standards with the greatest impact for your business model. IFRS 15 (revenue recognition) and IFRS 16 (lease accounting) are often critical. For IFRS 16 in particular, prepare a financial communication plan for your banking partners to explain the mechanical increase in debt, and consider renegotiating certain banking covenants if necessary.

Subsidiaries of International Groups

Capitalize on the parent group's experience: obtain their IFRS manuals, reporting tools, and engage IFRS experts from headquarters. Ensure that locally chosen accounting options are consistent with the group's. If your switch follows an acquisition by an IFRS group, draw on the new shareholder's steering capabilities to complete the project efficiently.

Conclusion

Transitioning to IFRS standards is an ambitious undertaking, often compared to a true enterprise-wide project. By methodically following the phases of diagnostic, design, implementation and publication, a group maximizes its chances of a smooth conversion.

Each step builds the foundation: the diagnostic establishes a solid starting point by identifying gaps and measuring stakes; design provides tailored solutions and choices; implementation brings these solutions to life by equipping and training the organization; finally, publication crowns the effort by producing reliable, audited IFRS financial statements.

Ultimately, adopting IFRS is an investment that, while demanding, can prove highly beneficial: enhanced comparability and credibility on the international stage, easier access to new capital, and improved overall quality of financial information produced.

Continue reading.

Receive Altesia analyses on consolidation, IFRS transition and finance transformation, straight to your inbox. One publication per month, nothing more.

- ✓1 email per month

- ✓Unsubscribe in 1 click

- ✓No third-party sharing